A slower start to the year

Rural property sale volumes for Q1 2024 were down 44% nationally on Q1 2023. The sharpest declines were in Victoria and Tasmania which were down 61% and 87% respectively, with these states having particularly dry starts that played on some buyer’s minds along with high interest rates and record farmland values.

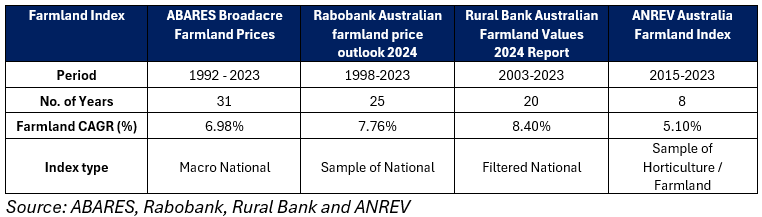

How has Australian farmland performed over the long term?

Australian farmland values have remained remarkably resilient over the last decade. The appreciation in land values has been one of the key reasons for investing in rural property and created significant wealth for landowners. This is highlighted by the high single digit compound annual growth rates (‘CAGR’) as reflected by most farmland growth indexes. Some high rainfall areas and key cropping regions exceeded these levels.

# Note the indexes vary widely in their approach to data cleansing, data analysis, duration, and source data (sales or valuations). All these factors account for a range of index results.

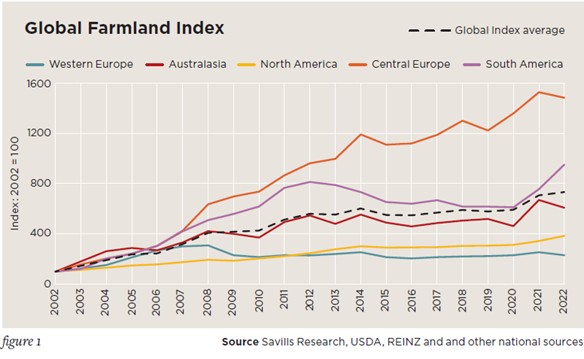

Globally, Australian farmland has performed well. In 2023 Savills prepared a Global Farmland Index based on 15 key agricultural markets, converted to US Dollars. On average the regions produced a CAGR of 10% with Australia close to the index average. In 2021 Australia experienced the second highest annual growth rate before tapering in 2022.

What is driving farmland values?

The long-term fundamentals of farmland values remain supportive however like all markets, values are exposed to fluctuations. We look how the key drivers of value (interest rates, agricultural production, and agricultural prices) will perform in the second half of 2024.

Interest rates

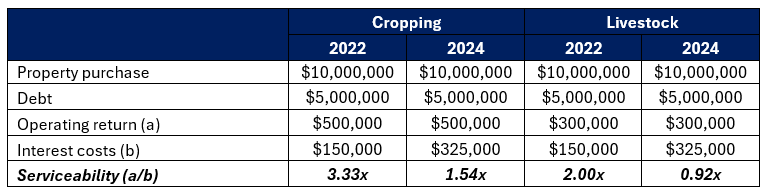

Investment in rural property slows when interest rates rise. The farmland market has been driven by the ‘neighbour to neighbour’ segment, which rely on debt funding to complete most acquisitions. This makes them more sensitive to interest rate changes than cashed up buyers less reliant on debt.

As an example, a farmer borrows half the purchase price for a property acquisition under an interest only, variable rate loan. In 2022 they would have been paying around 2.00%. Today they are paying closer to 6.00% as interest rates followed the cash rate higher. This means the farmer is today paying 3 times more in interest costs annually than in 2022. More farm cashflow is required to service the debt and if the borrower was a livestock producer cashflow are just able to meet debt obligations.

# Note the example uses operating returns of 5% for cropping and 3% for livestock, and all in interest rates of 3.00% in 2022 and 6.50% in 2024.

Most lenders require a minimum serviceability buffer of 1.25-1.50 times i.e. operating profit needs to be 1.25-1.50 times higher than interest costs. This buffer seeks to cover any potential issues that arise e.g. production setback, lower commodity prices, higher interest rates (bank regulation requires the buffer to cover a 3% increase to current interest rates) and is vitally important given the variability of agricultural production. As interest rates increase the buffer decreases and borrowers have less margin for error.

We consistently get feedback that reduced serviceability is driving a ‘risk off’ mentality at the banks. This is making it harder for farmers to access debt to fund acquisitions. This drop off in appetite is heightened in some regions and commodities that are experiencing drier conditions and/or weak commodity prices.

On the other hand, cashed up buyers including corporate buyers and farmers with sound balance sheets, have become more active in the market over the past 12 months. Most of these buyers are less sensitive to interest rates given conservative levels of debt in their business and cash accumulated from profits in recent years. They continue to seek out opportunities for larger, blue-ribbon properties that have strong production credentials, but are disciplined and patient in waiting for the right opportunity.

Overall, until interest rates recede interest rates will continue to be a headwind for rural property values.

2. Agricultural production

Seasonal conditions drive agricultural production. The forecast is for wetter than average conditions for much of eastern and central Australia whilst it will be drier than average in parts of the north, west and south.

A positive outlook and widespread autumn-winter rain on the east coast has ABARES forecasting an increase in national agricultural production volumes in 2024-25. Crop production is the main driver, expected to be up 9% on last year as many farmers on the east coast experience one of the best starts to a winter crop in recent years. This is expected to drive appetite for farmland in the second half of the year. In drier regions, farmers will look to tighten their belts which could see farmland values contract/hold.

Irrigation water in many of Australia’s key irrigation districts is also relatively secure for the coming 24 months, supporting production levels. The main curve ball for water markets continues to be the Federal Government’s voluntary water buyback of 450GL. This is expected to see water prices increase by 10 to 20% as the government enters a market that has seen historically low volumes of entitlement trade. Based on previous buybacks this sets a new water price level in the market which remains after the buybacks stop given water has been taken out of the system.

3. Agricultural prices

It has been a mixed bag for commodity prices and on average the outlook is neutral. Accordingly, it is unlikely commodity prices will materially stoke rural property buyer appetite in the second half of 2024. ABARES June quarter 2024 agricultural commodity report below outlines the forecast annual change in production values between 2023-24 and 2024-25.