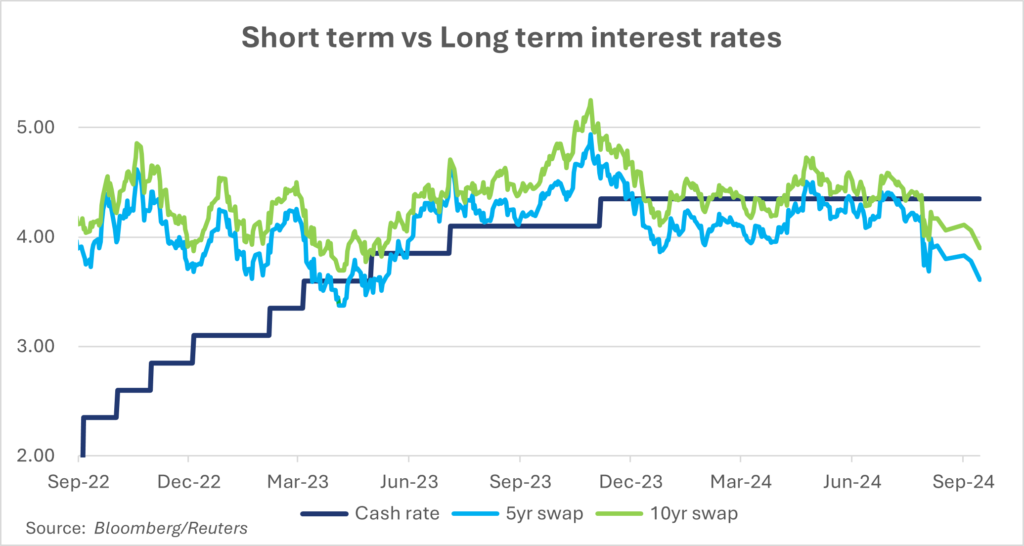

Recent concerns about the economic outlook have caused the inversion to steepen and extend further, making longer-term fixed rates more appealing. The current interest rate swap for 5 years is 3.61% and 10 years 3.90%, both sitting well below the RBA cash rate of 4.35%. Borrowers now have an opportunity to lock in historically attractive long-term rates and achieve immediate savings on interest costs.

In Australia inflation remains sticky and there is a risk it will rise in the year ahead, driven by record low unemployment and wage growth above 4%, record government spending, high energy costs, impacts of deglobalisation, etc. This could see the yield curve steepen and there is a high probability the RBA will hold rates at a higher level than expected for a considerable period.

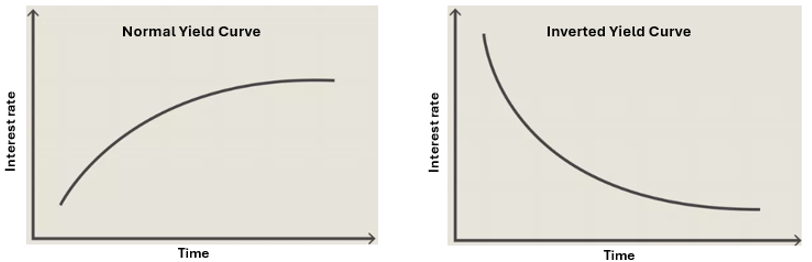

Yield curve inversion

The interest rate yield curve is a key economic indicator of expectations around future economic growth and inflation. Economies are cyclical and move through periods of growth, retraction and then expansion again. In a growing economy, the yield curve typically slopes upward, with long-term interest rates higher than short-term rates. This premium accounts for the greater uncertainty and risks associated with lending over a longer period.

In a slowing economy, the yield curve inverts, sloping downward as short-term rates become higher than long-term rates. Inversion is less common but one of the most reliable indicators of an impending economic downturn. It has historically preceded major recessions, including the early 1990s and the Global Financial Crisis. An inverted curve signals expectations that short-term interest rates will need to remain elevated to curb inflation and slow economic growth before eventually being lowered to stimulate a weakening economy.

Although an inverted yield curve typically signals a recession, there is often a time lag between the inversion and the onset of economic downturn, ranging from a few months to several years. An inversion however doesn’t always lead to a full-blown recession. Sometimes the “Goldilocks” scenario, where economic growth merely slows without triggering a recession, can occur – a situation economists and central bankers dream of.

Like good seasons and high commodity prices, yield curve inversions are temporary, and interest rates eventually return to the more typical upward-sloping curve. The current inversion which first appeared in March 2023 has been prolonged. There was a brief period when the curve reverted to a normal shape, driven by optimism that inflation was only a temporary issue. This optimism faded when the Reserve Bank of Australia (RBA) raised the cash rate by 25 basis points to 4.35% in November 2023. Since then, the inversion has deepened and extended.

Following the RBA’s move, the 5-year interest rate swap, which had been flat with the cash rate, dropped to a peak discount of 0.74% this week. Similarly, the 10-year swap, which was trading at a 0.30% premium to the cash rate prior to the RBA increase, has reached a discount of 0.45%. Interest rates beyond 10 years are now also trading below the cash rate as well (30-year interest rate swap is 3.98%).

Opportunity for borrowers

Farmers generally take a ‘long’ position, basing decisions on long term thinking and convictions, rather than short term market fluctuation. Similarly interest rate strategies should align with a farmer’s long-term financial goals.

During COVID-19, many borrowers deviated from their usual interest rate strategies. Although interest rates hit record lows, the steep yield curve discouraged borrowers from locking in long-term rates. At the time, the premium between the cash rate and the 5-year interest rate swap reached 3.54%, while for 10-year swap it was 3.69%. With shorter-term fixed rates offering a smaller premium, many borrowers opted to lock in rates for just 2-3 years.

The current interest rate yield curve looks more like a rollercoaster ride but with a distinct inverted trend. The RBA has signaled that it does not plan to reduce the cash rate in 2024, and markets remain concerned about stubborn inflation. This is reflected in higher short-term rates, before fears around a slowing economy push longer-term rates lower.

Globally, higher cash rates are starting to cool inflation, and several central banks have begun cutting rates. The US is expected to follow suit in September. This reduction in short-term rates should see their inverted yield curves return to a more normal upward slope.

Australia is an outlier to most developed nations, as it has a relatively low cash rate but higher inflation. Some cracks are appearing in the economy, however the challenge for borrowers is predicting how quickly inflation will fall and short-term rates can be paired back.

If a return to a normal yield curve is expected soon, staying on short-term rates may be a sensible strategy. However, the risk is that inflation persists for longer than expected, and the RBA keeps the cash rate higher for long. In that case, locking in longer-term fixed rates would be beneficial.