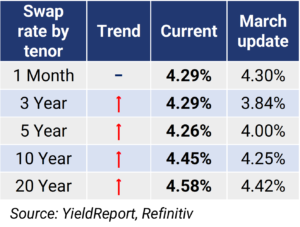

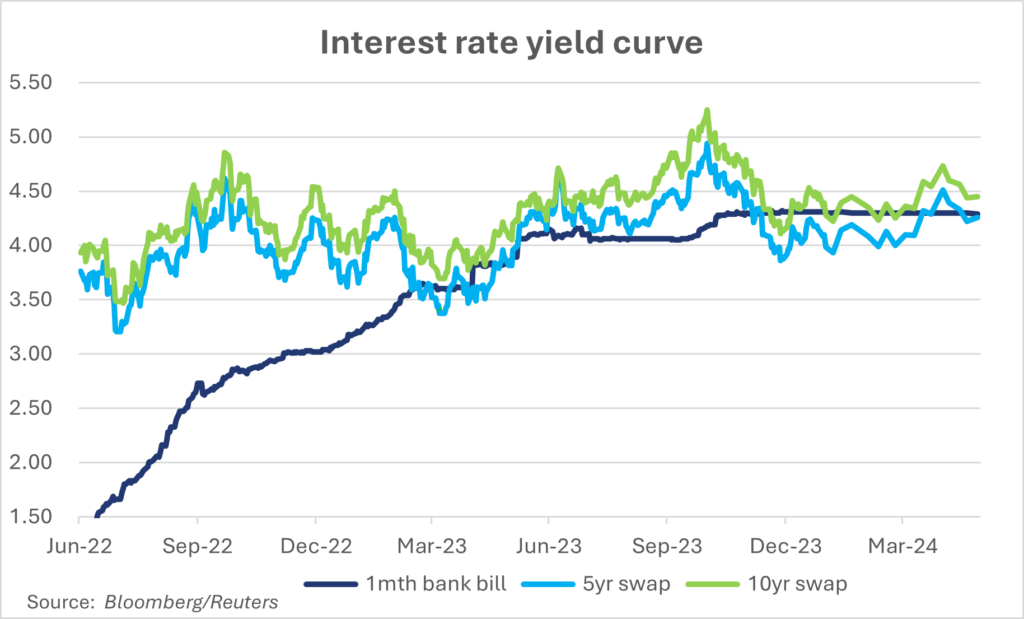

Interest rates

- It has been an eventful few months

for interest rates since our March update. Hopes of rate cuts this year were dashed, with central bankers signalling an openness to raising rates to combat inflation.

for interest rates since our March update. Hopes of rate cuts this year were dashed, with central bankers signalling an openness to raising rates to combat inflation. - This drove interest rates materially higher (although not quite to the peaks of last year).

- Borrowers should not assume the RBA won’t raise rates. The 3-to-5-year fixed rates, which sit below short-term rates, offer interest rate protection against the risk that rising inflation forces the RBA to lift the cash rate.

Note: Foundation Agri Finance price loans based on the current Australian Dollar Interest Swap Rate plus a customer margin. Please contact the team to discuss our competitive fixed-rate options.

What we’re hearing

Slower start to the year for property sales – Rural sale volumes for Q1 2024 are down 44% nationally on Q1 2023. Reflecting a combination of elevated land values, higher interest rates, softening commodity prices and mixed rainfall. The sharpest declines were in Victoria and Tasmania which were down a 61% and 87% respectively.

Disciplined buyers are taking their time to closely analyse an acquisition business case to make sure the numbers stack up, and are less willing to take a punt if there is limited upside. This is a significant change in behaviour from recent years when abundant and cheap debt made it easier to buy assets and meet interest costs. There are still plenty of farmers with the appetite and financial strength to grow, but they are patiently waiting for the right opportunity.

Banking relationships just not what they used to be – Many long-term clients are lamenting the decline in quality of the relationship with their bank. It is now more about ticking compliance boxes and less about adding value. Regular changes in relationship managers don’t help either.

The other common compliant is a ‘loyalty tax’ where long-term clients are on less competitive deals. The sharpest pricing and terms are reserved for new clients. According to the Reserve Bank of Australia the loyalty tax for existing business clients was on average 0.21% higher than new clients, and it got out to as much as 0.51%. This means an existing client’s interest bill could be 4-9% larger than a new client. In a tight margin business like agriculture, it all adds up.

Mixed bag for croppers – the summer crop wrapped up to mixed results and for northern growers on the east coast, the winter crop is off to a favourable start. Good moisture profiles and recent storms has cereal crops out of the ground. Larger chickpea plantings are going in as prices surge with the suspension of the Indian import tariffs. For Victoria and South Australia, it is a different story and many farmers are dry planting and hoping for rain. Similarly, the Western Australia crop hangs in the balance. Good rainfall is forecast across these regions through late May and early June, which if received would be highly beneficial.

It has been a very interesting few weeks for market strategists with the equity and bond markets simultaneously rallying after economic data confirmed that inflation is increasing, and the economy remains robust. This interpretation of the key data releases deserves some explanation as it flies in the face of actual market outcomes.

Global:

The US Producer Price Index (“PPI”) data at +0.5% for April was much stronger than expected at both the core and headline levels. There were downward revisions to prior months so that year on year the core PPI was 2.4%, in-line with expectations. The stronger price momentum suggests that wages are now feeding into producer prices, and these are being passed onto the buyers.

The latest CPI data was interpreted very favourably by the markets because after three months of upside surprise the result was in line with expectations. There was always an expectation that the CPI data would show a decline in April for seasonal reasons so the market’s reaction here is puzzling. When you look at the super core inflation level, which excludes shelter costs that are still increasing at 5.5% pa, it shows that underlying inflation actually rose in April to 4.7%pa.

The truth here is that inflation is still rising despite all the rate increases and the rise in the USD over the past 18 months. The market has been wrong about inflation since November last year.

Australia:

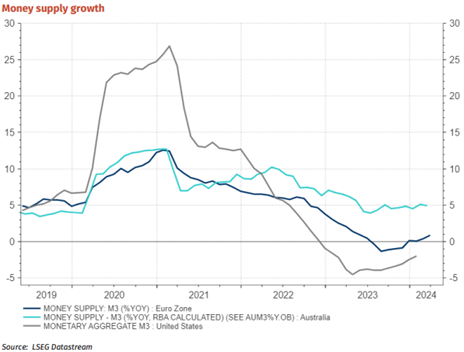

What the markets are failing to realise, and the RBA and Treasury are hypocritically ignoring, is that inflation in Australia will now begin to rise, driven by a wage price spiral. There are 3 overwhelming reasons for this:

- The RBA has not achieved negative money supply growth like the European Central Bank and the US Federal Reserve;

- The Federal and State Governments are still increasing fiscal expenditure which increases aggregate demand;

- Unemployment remains well below the 4.5% estimate of full employment and wages growth is running at 4% pa. Historically and reportedly the RBA has stated that wages growth needs to be no higher than 3% (and that is with an assumption of labour productivity being positive) if its 2-3% inflation target is to be achieved.

Quote of the update

“In every bull market, whether it is IBM or oats, the bulls always seem to come up with reasons it must go on, and on and on.” – Jim Rogers, American investor.

We do not include specific commodity price or seasonal updates as this is not out expertise.

If you would like to be added to the mailing list to receive the updates directly to your inbox, please fill in the form on the contact page and we will be in touch.