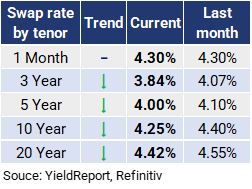

Interest rates

- Despite

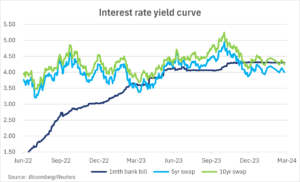

weekly volatility driven by a market jumping from one economic data release to the next, interest rates really haven’t changed much since November 2023. –

weekly volatility driven by a market jumping from one economic data release to the next, interest rates really haven’t changed much since November 2023. – - We are seeing interest in 5 year fixed-rate loans which are cheaper than short-term rates and provide certainty for borrowers until things settle down and the longer-term economic direction is clearer.

Note: Foundation Agri Finance price loans based on the current Australian Dollar Interest Swap Rate plus a customer margin. Please contact the team to discuss our competitive fixed-rate options.

Global:

The last mile of taming inflation is lengthening. Stronger than expected US CPI and Producer Price Index (PPI) for February stoked fears of a later than expected easing cycle by the Federal Reserve. The data highlighted the issues of rising fuel costs, further enhanced by a rising oil price last week, and strong wage growth now seeping into services prices to create a wage price spiral. Other data showed a resilient economy which also gives reason for a pause. Despite this, the market is still forecasting 3 rate cuts in 2024. The market may well suffer a rude awakening shortly.

2024 is an election year for the US and many Europeans, with a record number of electoral ballots scheduled. The easing of inflation pressures in the Euro area does give the European Central Bank some room to move on rates this year but it is unlikely to move prior to the June Euro Government elections. The Federal Reserve will also be more cautious about cutting rates too close to the Presidential election so if a rate cut does not occur by May we see them on hold until the December meeting. This will force the markets to adjust their rate cut expectations and hopefully focus back upon the fiscal expenditure plans of both parties.

Australia:

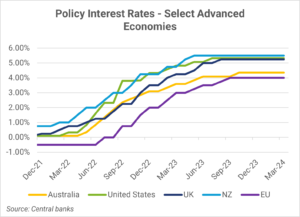

As we expected the RBA left the cash rate on hold at the March meeting. It is still remarkable to read how many economists are confident that the RBA will be cutting rates in the months ahead.

Unemployment is still below the full employment level; wages growth is only just gaining real momentum and we have what will certainly be an expansionary Federal Budget in May.

Globally Australia was late to the cash rate increasing party and remain below other advanced economies (aside from the EU which has dealing with prolonged economic malaise). Expect the RBA to continue lagging the field.

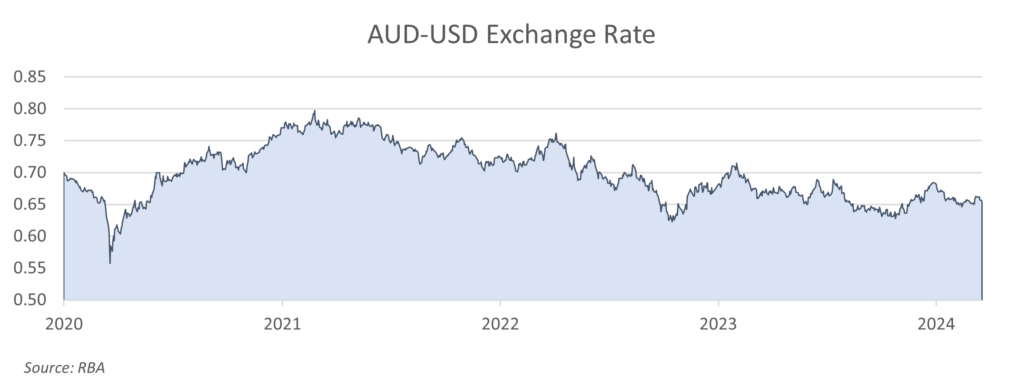

One to watch is the Australian dollar. The currency has been remarkably stable since the violent sell off at the onset of the pandemic in March 2020.

Three key reasons why this currency stability may be challenged this year include:

- The appointment of the new RBA interest rate setting Board reduces the central banks perceived and actual independence and this damages the market’s faith in its ability to control inflation.

- The falling iron ore price should shortly begin to impact the Australian current account outcome. It should not impact Federal Budget forecasts as the Australian Treasury had absurdly low iron ore price forecast of US$55 tonne in last year’s budget, but it will mean that actual tax revenue falls in the year ahead.

- The market does not believe the RBA will have the stomach to raise rates even if inflation surprises to the upside and is in fact still predicting three interest rate cuts. If inflation begins to rise in Australia and the RBA does not increase rates, then the market will devalue the currency so watch the Aussie dollar not bond yields for the next signal on the direction of RBA policy.

Quote of the update

“There is no benefit in an unhealthy river” – Paul Thompson, director Agribusiness Australia

We do not include specific commodity price or seasonal updates as this is not out expertise.

If you would like to be added to the mailing list to receive the updates directly to your inbox please fill in the form on the contact page and we will be in touch.