In Australia most borrowers can fix rates up to five years, however this normally only locks in the underlying cost of funds. The actual all up interest rate paid by a borrower is still uncertain as lenders have flexibility to adjust the customer margin which is charged on top of the cost of funds. This makes it difficult for borrowers to accurately predict and budget interest payments. In addition, the trend towards shorter loan periods has made it difficult for borrowers to match the investment horizon of a longer-term asset such as rural property, with a committed loan facility of a similar duration.

Is there an opportunity in Australian agriculture for long-term fixed-rate loans?

Figure 1: Major Bank’s Funding Composition

According to the Reserve Bank of Australia’s (RBA) statistics, the banks control 95% of the agricultural debt market and typically source most of their funding from cheaper, shorter-term options like domestic deposits and short-term debt as depicted in Figure 1. This makes it riskier to offer long-term fixed-rate loans given bank margins can become squeezed if there are increases in short-term funding costs. The banks also need to meet more onerous capital requirements that make the cost of funding longer loan periods more expense and less competitive in the market. The result is a shift to shorter loan periods of less than five years.

Non-bank lenders have more options to source capital from a range of different sources including investors focused on capital preservation and long-term returns. This makes long-term fixed-rate mortgage-backed loans highly attractive.

A long-term fixed-rate loan typically has a duration exceeding three years (possibly extending up to 30 years), during which the interest rate remains constant. When considering a long-term fixed-rate loan a business needs to assess how the financing options aligns with their specific requirements and objectives.

What are the benefits of long-term fixed-rate loans?

Interest rate certainty: The interest rate charged is locked in for the duration of the loan, so a borrower knows what the cost of the loan will be for the whole loan period.

Funding certainty: The loan is fully committed for the life of the loan and the loan terms locked in upfront, so a borrower knows they have the funds secured and the terms on which itis being offered. This contrasts with shorter-term loans that need to be renewed more regularly, exposing borrowers to a lender’s prevailing appetite at the time it comes to renew a loan and how this view shapes what is considered appropriate pricing and loan terms. For a borrower on a three year loan facility this would mean the uncertainty of five different renewals vs a 15-year fixed-rate loan that is locked in at the start.

Renewal costs: Each time a short-term loan is extended there are costs involved. This cost is significantly reduced on long-term loans which normally have initial establishment costs and no ongoing fees.

Match funding: Aligning long-term asset investment with long-term funding. Farms are long-term assets and in the case of family operations, generational assets. Therefore, having funding committed for the long-term gives borrowers’ confidence they can make asset investments work over the long-term.

What are the disadvantages of long-term fixed-rate loans?

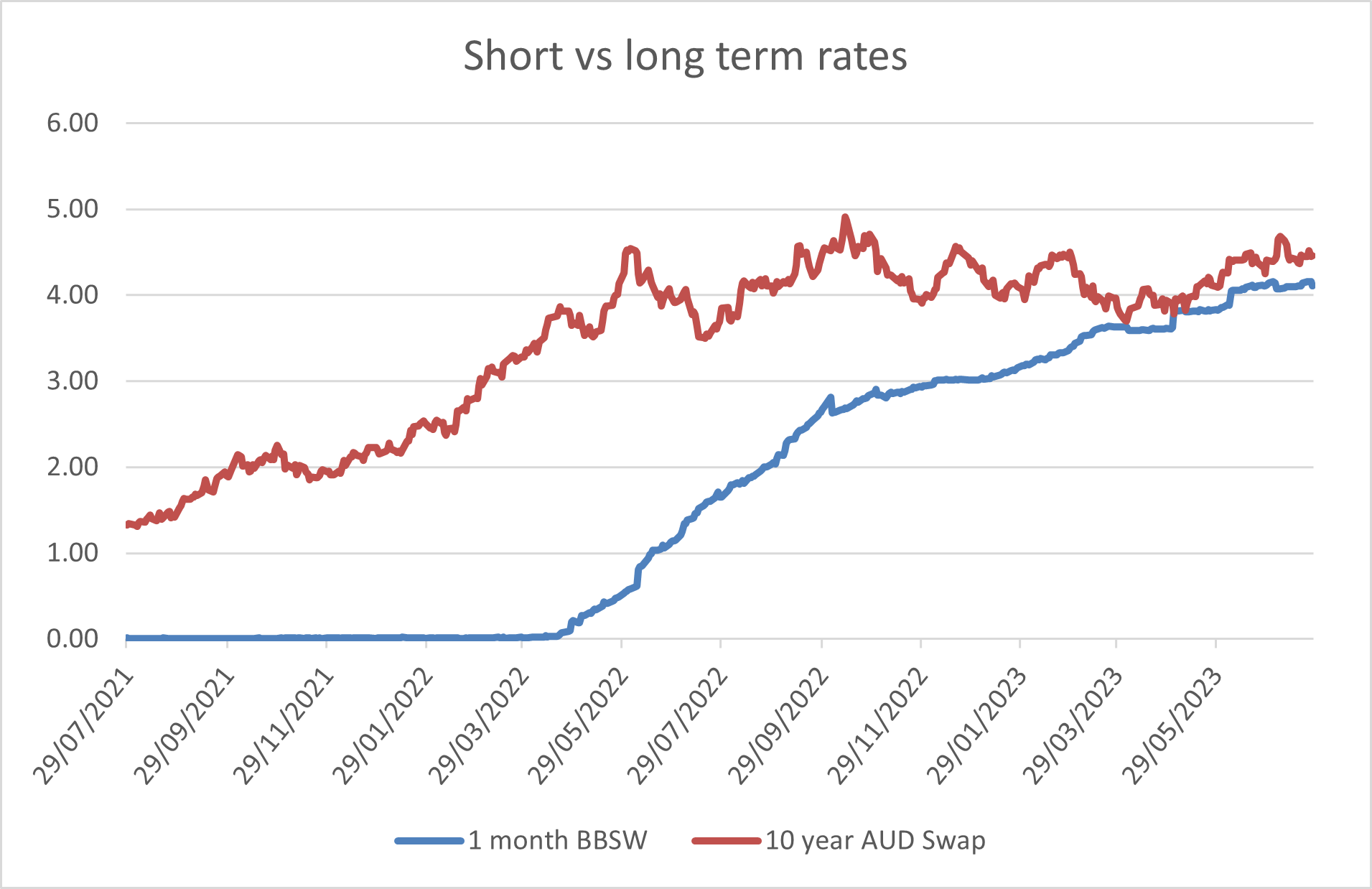

Figure 2: short vs long term rates (note: excludes borrower margin) Source: RBA and Bloomberg

Higher rate: A premium is generally charged for the stability and security of a long-term deal, however the difference moves with the overall interest rate environment. Figure 2 below highlights how the premium between short and longer-term rates has moved over the last two years. The gap peaked at just under 4% in June 2022 before declining to ~0.30% currently.

Reducing interest rates: If interest rates go lower the borrower does not receive the benefit given the rate is fixed for the life of the loan.

Less flexibility: There may be cost associated with early repayments of a loan if you want to sell property or pay off a substantial amount.

What does this mean in practice?

There are several of examples where the benefits of long-term fixed rate loans make sense. The acquisition of a property can be a key milestone for a family farming business, bringing with it both long-term growth opportunities and risks. Knowing the cost of funding and having the certainty of a committed loan facility can provide the confidence needed to make the investment.

When developing farming assets there can be a lag between the initial outlay of capital and realising the upside in production. For permanent plantings such as almonds it can take up to five years before the trees are cashflow positive. A long-term fixed-rate loan enables more accurate budgeting particularly during the start-up phase when cashflow is tighter.

Succession in a family farming business often creates uncertainty and risks as the business/assets transition to the next generation. Those remaining in the business can be required to inherit the existing debt and take on new debt to payout parents and other siblings. Having finance committed for the long-term and knowing exactly what the interest costs will be can provide the certainty needed to make the succession achieve its goals.

In summary, long-term fixed-rate loans can be an important funding option to help borrowers achieve greater certainty for the future – providing farmers with the support to make the long-term investment decisions necessary for their business.